What is blockchain? 🧬

Blockchain is a kind of database that uses a public ledger to record transactions without requiring a third party to validate each operation. It’s distributed via a peer-to-peer network and made up of data blocks that are linked together to form a continuous chain of immutable records. Each computer in the network keeps a copy of the ledger to avoid a single point of failure. Blocks are inserted sequentially, and they are permanent and tamper-proof.

The Birth of Blockchain: A Brief History 🎂

1979: One of the early pre-blockchain technologies is the Merkle tree, named after computer scientist and mathematician Ralph Merkle. He described tree authentication, which is a method of distributing public keys and digital signatures. He eventually patented this concept as a way to provide digital signatures. It defines a data structure for checking individual records.

1982: David Chaum suggested a vault system for creating, managing, and trusting computer systems amongst mutually suspicious entities. He is also credited with creating digital cash, and in 1989 he launched DigiCash.

1991: Stuart Haber and W. Scott Stornetta wrote an essay about how to timestamp digital documents to prevent them from being backdated or forward-dated. The objective was to make the document completely private without necessitating record-keeping by a timestamping service. Haber and Stornetta extended the architecture to include Merkle trees, allowing several document certifications to reside on a single block.

1999: Napster, the peer-to-peer file sharing program, popularised the P2P networks. Some claimed that Napster was not a real peer-to-peer network since it required a centralised server. However, the service did contribute to the revival of the P2P network by allowing the creation of a distributed system that could benefit from the compute power and storage capacity of thousands of machines.

2004: Hal Finney, a cryptographic activist, introduced the “Reusable Proof of Work” digital payment concept. This move was a game changer in the history of Blockchain and Cryptography. This system assists others in solving the Double Spending Problem by registering token ownership on a trustworthy server.

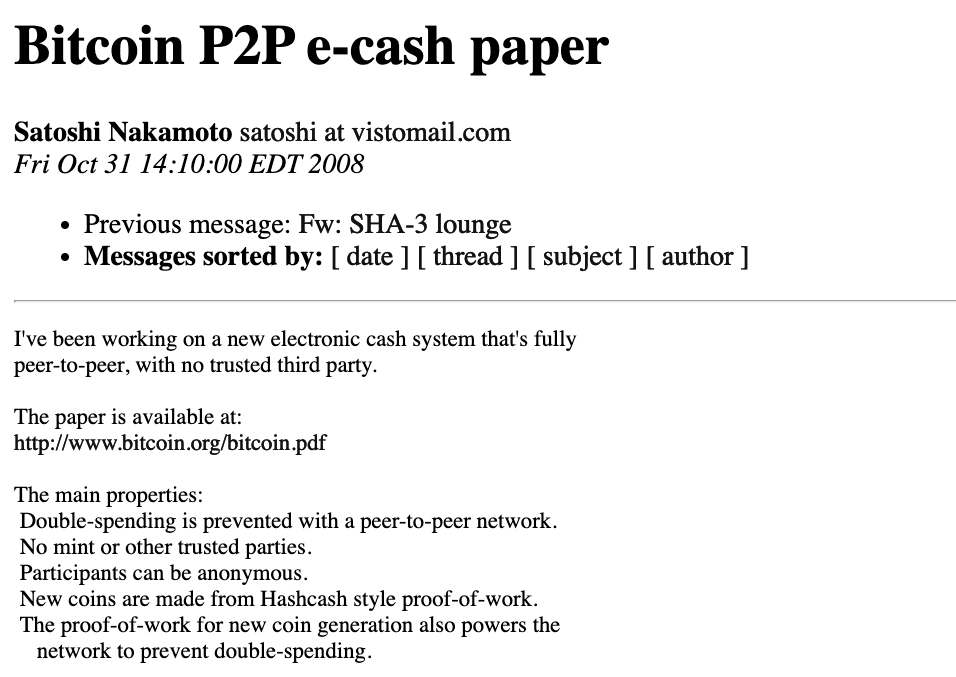

2008: In 2008 at the height of the financial crisis, a mysterious figure released a message to the world. This message was about Bitcoin, a new electronic cash system that was fully peer-to-peer without any third party involved.This message was written by Bitcoin’s creator, Satoshi Nakamoto, who would stop communicating with the world only a few years later.

According to the white paper, blockchain technology will enable safe, peer-to-peer transactions without the need for trusted third parties such as banks or governments. Although Nakamoto’s true identity remains unknown, there have been several hypotheses.

Nakamoto’s design also included the concept of a “chain of blocks,” which allowed blocks to be added without needing to be signed by a trusted third party. Nakamoto characterised an electronic coin as a “chain of digital signatures,” with each owner transferring the coin to the next owner by “digitally signing a hash of the previous transaction and the next owner’s public key and adding these to the end of the coin.”

2009: Cryptocurrency was created during the Great Recession, when the government poured massive sums of money into the economy. The value of Bitcoin was less than a cent back then. Nakamoto mined the first Bitcoin block, which validated the blockchain idea. The Genesis block (also known as block 0) contains 50 bitcoins. Nakamoto made Bitcoin v0.1 available as open source software through the web site SourceForge. Bitcoin is now on GitHub.

In the spirit of cryptocurrency as money with fixed supply, Nakamoto set up a system to ensure the number of bitcoin mined won’t ever exceed 21 million.

On 2010 May 22, Bitcoin made history when a programmer Laszlo Hanyecz paid 10,000 bitcoin for two delivered Papa John’s pizzas. The two pizzas back then were valued at about $40, a transaction that would balloon to a value of more than $260 million at today’s bitcoin price level.

Key features of Blockchain 🗝️

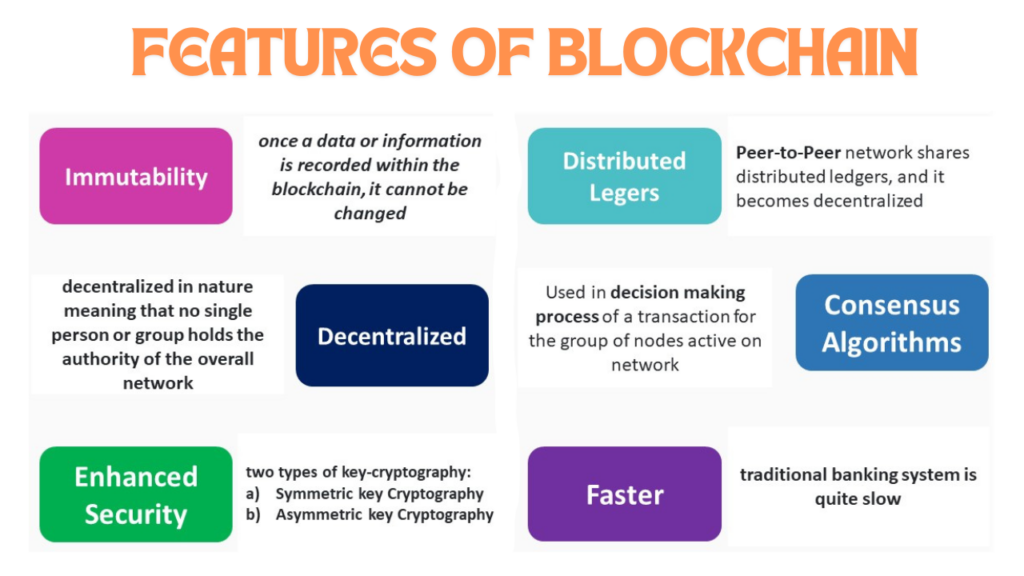

📌 Immutability

There are various fascinating blockchain aspects, but “immutability” is without a doubt one of the most important properties of blockchain technology. But why isn’t this technology corrupted? Let’s start by integrating blockchain with immutability.

Immutability refers to something that cannot be changed or altered. This is one of the most important blockchain aspects for ensuring that the technology remains as it is: a permanent, unalterable network. But how does it remain that way?

Blockchain technology operates slightly differently than traditional financial systems. Rather than depending on centralised authority, it assures blockchain functionality via a network of nodes.

Each node in the system has a copy of the digital ledger. To add a transaction, every node must verify its authenticity. If the majority believes it is correct, it is added to the ledger. This fosters openness and prevents corruption.

No participant can tamper with a transaction once someone has recorded it to the shared ledger. If a transaction record includes an error, you must add a new transaction to reverse the mistake, and both transactions are visible to the network.

So, without the approval of the majority of nodes, no transaction blocks may be added to the ledger.

Once transaction blocks are recorded to the ledger, they cannot be changed again. Thus, no user on the network will be able to modify, remove, or update it.

📌 Decentralized

Blockchain relies on a decentralised network of computers known as nodes. These nodes coordinate to validate and record transactions. Decentralisation guarantees that no single entity has complete control over the system, making it resistant to censorship and single points of failure.The network is decentralized meaning it doesn’t have any governing authority or a single person looking after the framework.

This is a vital aspect of blockchain technology that functions flawlessly. Let me simplify it. Blockchain puts users in a plain position. Because the system does not require any regulating authority, we may access it over the internet and keep our assets there.

You can store anything, including bitcoins, vital papers, contracts, and other significant digital assets. And, because to blockchain technology, you will have direct control over them via your private key. As you can see, the decentralised system restores the ordinary people’s control and rights over their possessions.

Why is it so valuable?

Less Prone to Breakdown: Because decentralisation is one of the defining characteristics of blockchain technology, it can withstand any hostile assault. This is because hacking the system is more expensive and difficult to do. So it’s less likely to fail.

User Control: Decentralisation gives people more control over their possessions. They do not need to rely on a third party to preserve their assets. They can all do it on their own.

Less Failure: Everything on the blockchain is completely organised, and because it does not rely on human calculations, it is extremely fault-tolerant. As a result, inadvertent system breakdowns are an uncommon occurrence.

No Third-Party: The decentralised nature of the technology results in a system that does not rely on third-party firms; no third-party, no extra danger.

Zero Scams: People cannot defraud you since the system is based on algorithms. No one may use blockchain for personal advantage.

Authentic Nature: Because of this, the technique is unique and suitable for any type of individual. And hackers will have a difficult time breaking it.

Transparency: The decentralised nature of technology results in a transparent profile for each participant. Every modification to the blockchain is visible and makes it more tangible.

📌 Security

Because it eliminates the need for a central authority, no one can easily modify any aspect of the network to their advantage. Using encryption adds another degree of protection to the system.

But how can it provide so much security compared to other technologies?

It’s incredibly safe since it uses a unique disguise – cryptography.

Cryptography, in addition to decentralisation, provides consumers with an extra degree of security. Cryptography is a complicated mathematical procedure that serves as a barrier against attackers.

Every bit of data on the blockchain is hashed cryptographically. Simply said, the information on the network conceals the real nature of the data. In this procedure, any input data is passed through a mathematical algorithm that generates a different type of result, but the length is always fixed.

You may think of it as a unique identifier for all data. Each block in the ledger has a unique hash and contains the preceding block’s hash. So, modifying or attempting to tamper with the data will require changing all of the hash IDs. That’s very much impossible.

You will have a private key to access the data, but a public key to conduct transactions.

Hashing is a very sophisticated process that cannot be altered or reversed. Nobody can generate a private key from a public key. Furthermore, a single modification in the input might result in an entirely new ID, therefore minor adjustments are not a luxury in the system.

If someone wishes to corrupt the network, he or she must change all of the data stored on each node in the network. There may be millions of people, each with the same copy of the ledger. Accessing and hacking millions of machines is virtually difficult and expensive.

That’s why it’s one of the most useful blockchain characteristics. Because it is difficult to circumvent, you will not have to worry about hackers stealing all of your digital possessions.

📌 Consensus

To put it simply, consensus is a decision-making process for the network’s active nodes. Here, the nodes may reach an agreement rapidly and reasonably easily. When millions of nodes validate a transaction, consensus is definitely required for the system to function properly. You may conceive of it like a vote system in which the majority wins and the minority must support it.

Every blockchain flourishes due to consensus algorithms. The architecture is intelligently constructed, with consensus mechanisms at its heart. Every blockchain uses consensus to help the network make choices.

The lack of confidence in the network is due to consensus. Nodes may not trust one another, but they may trust the algorithms that power the system. That is why every network choice is a positive outcome for the blockchain. This is one of the advantages of blockchain characteristics.

There are several different consensus algorithms for blockchains throughout the globe. Each has an own approach to decision-making, and mastering prior methods brings errors. The architecture establishes a sphere of justice on the web.

However, to keep the decentralization going every blockchain must have a consensus algorithm, or else the core value of it is lost.

📌 Faster Settlement

Traditional banking systems are quite sluggish. After all settlements have been completed, it may take several days to finalise a transaction. It is also highly susceptible to corruption. Blockchain provides speedier settlement than traditional financial systems. This allows a user to transfer money reasonably quickly, saving a lot of time in the long run.

Blockchains are now extremely quick, and people may simply utilise them to transmit money to their loved ones abroad. Another amazing fact is the smart contract system. This allows for speedier contract settlements of any form. This is one of the most significant benefits of blockchain features today. And, with the third party taken away users may transmit money for a little price.

Blockchain technology enables the creation and execution of smart contracts, which are self-executing contracts that automatically execute when certain conditions are met. Smart contracts have the potential to revolutionize various industries by providing a secure and transparent way to execute contracts.

📌 Distributed Ledgers

The blockchain ledger is public and transparent, which means that anyone can access and view the transactions on the network. This makes it a highly transparent system that is resistant to fraud and corruption.

The distributed ledger responds very effectively to any suspicious behaviour or manipulation. Because no one can edit the ledger and everything updates quickly, it is simple to follow what is going on in the ledger with all of these nodes.

Here, nodes serve as ledger verifiers. If a user wishes to add a new block, others must verify the transaction before giving the green signal. This ensures the user’s fair involvement.

No one on the network can receive any particular benefits from the network. Everyone has to go through the appropriate methods before adding their blocks. It’s not like having greater authority means you’ll receive more privileges.

Every active node has to maintain the ledger and participate in validation.The removal of intermediates improves the system’s reaction time. Any modification to the ledger is reflected in minutes or even seconds!

What is a Block? 🎲

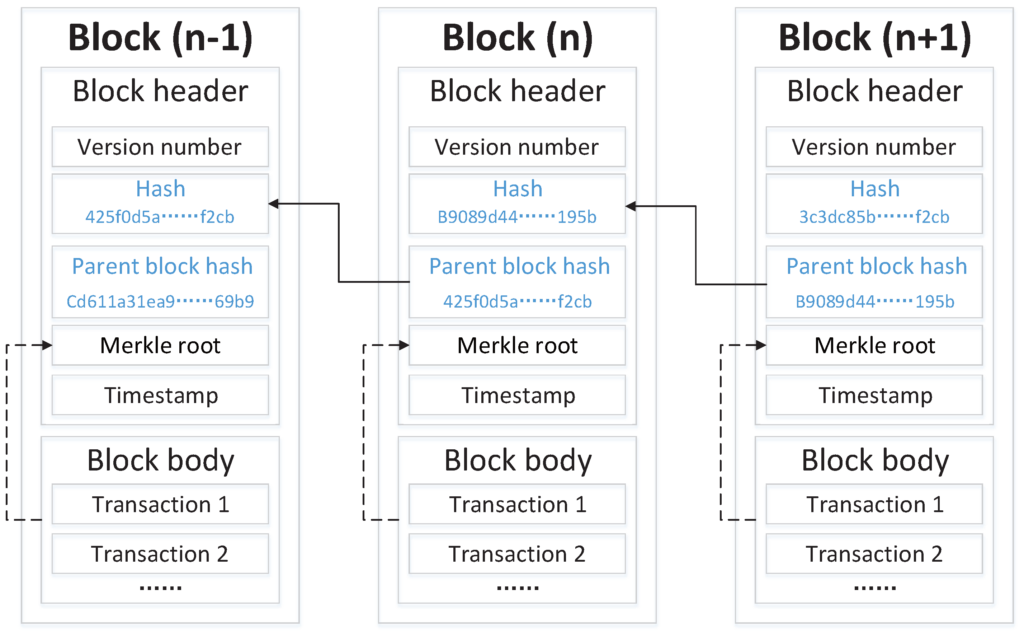

A block is a file in which data is stored and encrypted.Blocks are identifiable by lengthy integers that contain both encrypted transaction information from previous blocks and fresh transaction information.Before new blocks can be generated, the network must verify the information contained within them.Blocks and blockchains aren’t just utilised by cryptocurrency. They also have several additional applications.

The transactions made during a period are recorded into a file called a block, which is the basis of the blockchain network.A block contains information. A block contains a significant amount of information yet takes up little storage space. Blocks generally include these elements, but it might vary between different types.

For example block contains:

- Blocksize: Sets the size limit on the block

- Block header: Contains information about the block

- Transaction counter: How many transactions are stored in the block

- Transactions: A list of all of the transactions within a block

The transaction element is the largest because it contains the most information.It is followed in storage size by the block header, which includes sub elements like:

- Version: The cryptocurrency version being used (magic number)

- Previous block hash: hash of the previous block

- Nonce: A number the miner increases incrementally when hashing

- Timestamp: A timestamp to place the block in the blockchain

- Difficulty Target: Signifying the difficulty in generating a hash

- Different blockchains may contain more different headers

How Does Blockchain Work? ⚙️

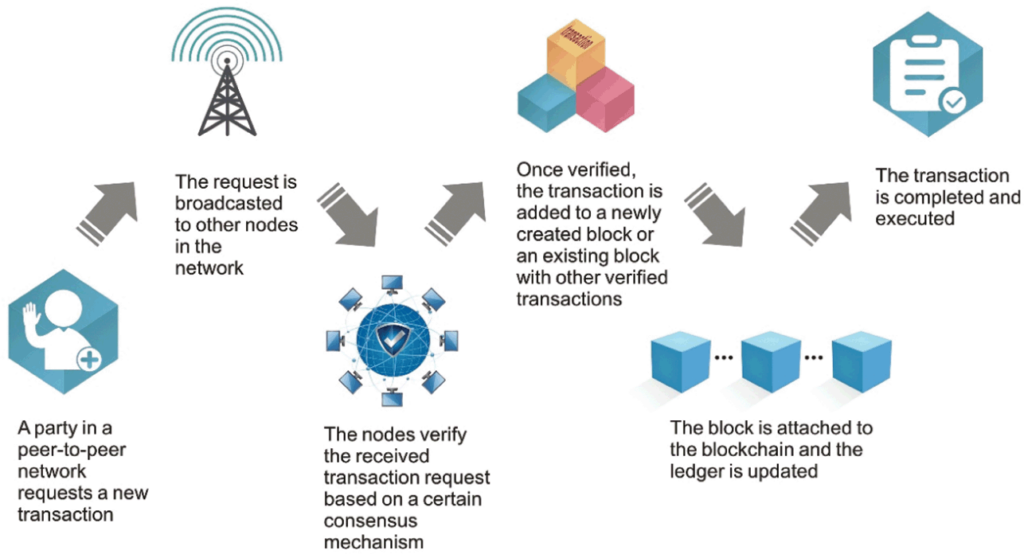

Facilitating a transaction: A new transaction is added to the blockchain network. All necessary information is double encrypted with public and private keys.

Transaction verification: The transaction is then routed through a global network of peer-to-peer computers. All nodes in the network will check the transaction’s legitimacy, such as whether a sufficient balance is available to complete the transaction.

Formation of a new block: In a normal blockchain network, there are numerous nodes and several transactions are validated at the same time. Once confirmed and declared authentic, the transaction will be added to the mempool. All validated transactions at a certain node create a mempool and such.

Consensus Algorithm: Nodes that compose a block will attempt to add it to the blockchain network, making it permanent. However, allowing each node to contribute blocks in this manner will disrupt the operation of the blockchain network. To address this issue, the nodes employ a consensus process to ensure that each new block added to the Blockchain is the only version of the truth that all nodes agree on, and that only a valid block is safely linked to the blockchain.

The node that is chosen to add a block to the blockchain receives a reward, which is why we call them “miners”. The consensus algorithm generates a hash code for the block, which is needed to add it to the blockchain.

Adding the new block to the blockchain: Once the newly formed block has received its hash value and been authenticated, it is ready to be added to the blockchain. Every block contains the preceding block’s hash value, which is how the blocks are cryptographically linked together to build a blockchain. A new block is added to the open end of the blockchain.

Transaction complete: Once the block is uploaded to the blockchain, the transaction is complete, and the information are permanently saved in the blockchain. Anyone may obtain the transaction details and confirm them.

Types of Blockchain 🎭

There are four main types of decentralized or distributed networks in the blockchain:

Public blockchain networks

Public blockchains are permissionless, allowing anybody to join them. Everyone on the blockchain has equal access to read, modify, and validate the blockchain. People typically utilise public blockchains to exchange and mine cryptocurrency such as Bitcoin, Ethereum, and Litecoin.

Private blockchain networks

Private blockchains, or managed blockchains, are controlled by a single organisation. The authority determines who may become a member and what privileges they have within the network. Private blockchains are only partially decentralised due to access limitations. Ripple, a business-focused digital currency exchange network, is one example of a private blockchain.

Hybrid blockchain networks

Hybrid blockchains mix aspects of private and public networks. Companies can run private, permission-based systems alongside public ones. In this way, businesses may regulate access to select data recorded on the blockchain while leaving the rest of the data public. They employ smart contracts to enable public members to determine whether private transactions have been completed. For example, hybrid blockchains can provide public access to digital cash while keeping bank-owned currency private.

Consortium blockchain networks

A set of organisations oversees consortium blockchain networks. Preselected organisations are responsible for maintaining the blockchain and setting data access permissions. Industries with several organisations that share aims and profit from shared responsibilities frequently prefer consortium blockchain networks. For example, the Global Shipping Business Network Consortium is a non-profit blockchain consortium dedicated to digitising the shipping sector and increasing collaboration among marine industry players.

Future of Blockchain Technology 🌱

- Blockchain technology has far-reaching applications across many industries.

- Blockchain is already used to facilitate identity management, smart contracts, supply chain analysis, and much more.

- The full potential of blockchain technology likely remains to be discovered, but it is likely to be used in conjunction with emerging technologies.

Finally, blockchain technology is altering how we store and handle data. Its decentralised and transparent architecture makes it more safe, efficient, and dependable than traditional databases. It has the potential to transform a variety of industries, including supply chain management, voting, finance, and healthcare. As technology advances, there will surely be new applications and use cases that we have not yet considered.

FAQ 💡

What is blockchain technology, and how does it work?

Blockchain is a decentralized digital ledger that records transactions across multiple computers in a secure and transparent manner. It works by grouping transactions into blocks, which are then linked together in a chain using cryptographic principles.

Why is blockchain considered a disruptive technology?

Blockchain is disrupting industries by eliminating intermediaries, enhancing transparency, and improving security. From finance to supply chain management, its decentralized nature is transforming traditional systems.

What are the key benefits of blockchain technology?

Blockchain offers numerous benefits, including enhanced security, transparency, immutability, and cost efficiency. It also enables faster and more reliable transactions.

What industries are being transformed by blockchain?

Blockchain is revolutionizing industries such as finance, healthcare, supply chain, real estate, and more. Its applications range from cryptocurrency to smart contracts and decentralized systems.

What are the challenges of implementing blockchain technology?

Despite its potential, blockchain faces challenges such as scalability issues, regulatory concerns, and high energy consumption. Understanding these hurdles is crucial for successful adoption.

How can businesses leverage blockchain technology?

These FAQs are optimized for SEO by incorporating relevant keywords like “blockchain technology,” “disruptive technology,” and “blockchain applications.” They also include internal links to your article, which can improve its search engine ranking and drive more traffic.

References 🔗

- https://hbr.org/2017/01/the-truth-about-blockchain

- https://www.weforum.org/agenda/2021/09/how-blockchain-can-transform-industries/

- https://www.mckinsey.com/business-functions/mckinsey-digital/our-insights/blockchains-occam-problem

- https://www.ibm.com/blockchain/for-business

- https://www.coindesk.com/learn/what-is-blockchain-technology/

{kind=link}